Many retirees are surprised to learn that Medicare premiums are not the same for everyone.

If your income is above certain thresholds, you may pay a Medicare premium surcharge called IRMAA (Income-Related Monthly Adjustment Amount). This surcharge can apply even if you have the exact same Medicare coverage as your neighbor.

Understanding Medicare IRMAA is critical because crossing an income threshold by even $1 can increase premiums for the entire year. For many retirees (especially those with $2M+ in net worth), IRMAA exposure becomes more common due to Roth conversions, RMDs, capital gains, and real estate sales.

We regularly meet retirees who say, “Nothing about our income changed, but our Medicare premiums jumped.”

The reason is almost always IRMAA.

In this guide we’ll explain what IRMAA is, how it works, how much it can cost, and strategies retirees use to reduce IRMAA exposure.

Table of Contents

What Is Medicare IRMAA?

Medicare IRMAA is an additional surcharge added to your Medicare premiums when your income exceeds certain limits.

IRMAA applies to:

- Medicare Part B (medical insurance)

- Medicare Part D (prescription drug coverage)

If IRMAA applies to you, you pay:

- the standard Medicare premium plus

- an income-based surcharge

These surcharges are per person, not per household.

How Medicare IRMAA Is Calculated (The 2-Year Lookback Rule)

Medicare IRMAA is based on your Modified Adjusted Gross Income (MAGI) from two years prior. This means decisions you make today quietly determine what you pay for Medicare two years from now.

Example: Your 2026 Medicare premiums are based on your 2024 tax return.

MAGI generally includes:

- ordinary income

- capital gains

- Roth conversions

- IRA withdrawals (including RMDs)

- pension income

- taxable Social Security (partially)

- tax-exempt interest (important for retirees holding municipal bonds)

This is why proactive planning matters. By the time IRMAA shows up, the income event already happened.

2026 Medicare Premiums: The Starting Point

For 2026, the standard Medicare Part B premium is $202.90 per month per person.

Part D is different because your base Part D premium depends on your plan, but IRMAA adds a separate monthly surcharge if your income crosses the thresholds.

IRMAA Income Cliffs

IRMAA works in cliffs, not gradual phases. Crossing an IRMAA income bracket by even $1 can push you into a higher Medicare premium level for the entire year.

For 2026, the first IRMAA tier (level 1) begins above:

- $109,000 (single)

- $218,000 (married filing jointly)

There are 5 IRMAA tier levels total. Each time you jump a level your premiums increase.

The Medicare Part B premium in 2026 ranges from:

- $202.90 per month (standard)

up to - $689.90 per month (highest IRMAA tier)

That means high-income retirees can pay more than $8,200 per person per year in Part B premiums.

Part D IRMAA adds an additional surcharge on top of your normal Part D plan premium. In 2026, Part D IRMAA amounts range up to roughly $90+ per month depending on income tier.

The $1 IRMAA Cliff Example (Why Planning Matters)

Let’s say a married couple has 2024 MAGI of:

- $218,000 = no IRMAA surcharge

- $218,001 = IRMAA surcharge kicks in

Once IRMAA applies, premiums increase for each spouse.

In 2026, moving into the first IRMAA bracket increases Medicare Part B premiums from $202.90 to $284.10 per person per month.

That is an increase of:

- $81.20 per month per person

- $1,948.80 per year for a married couple

Part D IRMAA also begins at that tier, adding an additional monthly amount per person.

Total IRMAA cost for the couple can easily exceed $2,000 in a year because their MAGI was $1 over the threshold.

This “cliff” effect is why IRMAA planning becomes a serious issue for affluent retirees, even if they don’t consider themselves “high income” in most years.

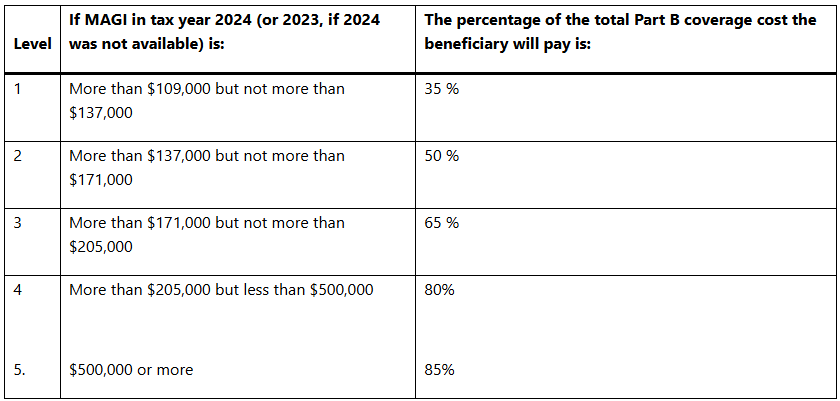

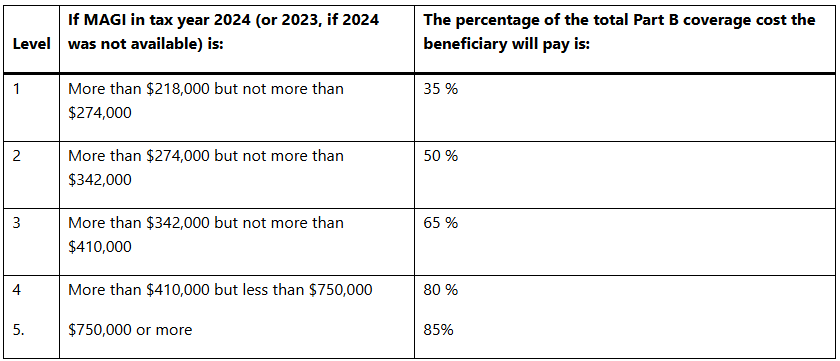

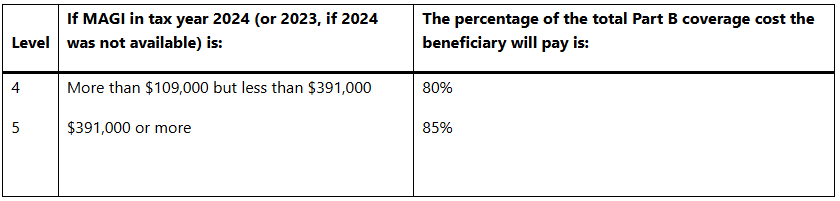

IRMAA Medicare Premium Income Thresholds

Tax filing status:

- single, head of household

- married, filing separately (but living apart for the entire year)

- surviving spouse with dependent child

Tax filing status: Married filing jointly

Tax filing status: Married, filing separately (but lived together at some time during the year)

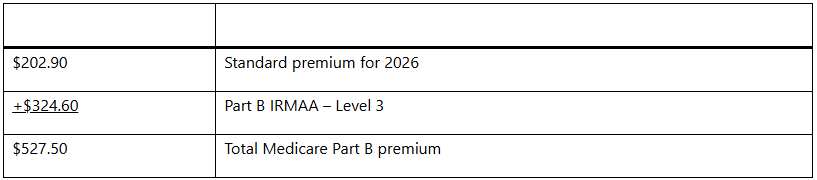

Example:

Common IRMAA Triggers for Retirees

Most IRMAA exposure doesn’t come from wages. It comes from financial decisions and one-time events:

Roth conversions

Large conversions increase MAGI and can push you across multiple IRMAA tiers.

Large IRA withdrawals or growing RMDs

As pre-tax accounts grow, RMDs alone can push retirees into IRMAA territory.

Capital gains

Selling rental property, concentrated stock, or highly appreciated assets.

One-time income events

Business sales, severance, special dividends, deferred compensation payouts.

How to Reduce or Avoid IRMAA (High-Impact Strategies)

There is no single way to eliminate Medicare IRMAA, but there are several proven strategies that can help reduce or manage exposure.

Use Qualified Charitable Distributions (QCDs)

If you are age 70½ or older, Qualified Charitable Distributions (QCDs) allow you to donate directly from an IRA to a qualified charity while keeping those dollars out of MAGI.

QCDs can help:

- Lower MAGI

- Reduce Medicare premium surcharges

- Satisfy RMDs in a tax-efficient way

For more information, see:

Qualified Charitable Distribution (QCD): Rules, Limits, and Common Mistakes

Coordinate Roth Conversions Across Years

Instead of converting a large amount in a single year, many retirees use a multi-year Roth conversion strategy designed to stay below:

- Target tax bracket ceilings

- IRMAA income ceilings

This approach often produces better long-term results than one large conversion.

For more information see:

A Guide to Roth Conversions

Manage Capital Gains Intentionally

Rather than selling assets only when convenient, retirees can:

- Spread gains across multiple years

- Use tax-loss harvesting when available

- Donate appreciated shares instead of selling

Intentional gain management can significantly reduce IRMAA exposure.

For more information see:

How Capital Gains Tax Works: 7 Important Facts

Use Donor-Advised Funds Strategically

Donor-advised funds can create large itemized deductions in years when income spikes, such as:

- Roth conversion years

- Real estate sales

- Business sales

These deductions may help offset MAGI and soften IRMAA impact.

For more information, see:

Itemizing and Bunching: A Smart Tax Strategy for Charitable Giving

Can You Appeal Medicare IRMAA?

Yes. If IRMAA is based on a year that no longer reflects your current income due to a life-changing event, you may be able to appeal using Social Security Form SSA-44.

Examples of qualifying events include:

- retirement

- death of a spouse

- divorce

- loss of income-producing property

At White Cloud Wealth Management, we frequently assist our clients with appealing Medicare IRMAA.

Medicare IRMAA Is a Tax Planning Issue, Not a Medicare Issue

This is the key takeaway:

Medicare premium surcharges are driven by tax decisions, not healthcare decisions.

That means:

- Roth planning

- IRA withdrawal strategy and RMD planning

- charitable giving strategies

- capital gains management

All directly influence Medicare premiums.

When these decisions are made in isolation, IRMAA is often the unintended cost.

Frequently Asked Questions About Medicare IRMAA

Does Medicare IRMAA apply to everyone?

No. IRMAA only applies if your income exceeds specific thresholds. Many retirees never pay IRMAA, but those who do can pay significantly more in Medicare premiums.

Is Medicare IRMAA permanent?

No. IRMAA is recalculated each year based on income. If your income decreases in future years, your Medicare premiums can also decrease.

Does IRMAA affect both spouses?

Yes. IRMAA applies per person, even though income is based on a joint tax return. Each spouse can be subject to their own surcharge.

Can charitable giving reduce IRMAA?

Yes. Strategies such as Qualified Charitable Distributions (QCDs) reduce MAGI directly. Donor-advised funds and donating appreciated stock can also help manage income in higher-income years when used intentionally.

Why didn’t my advisor or Medicare agent warn me about IRMAA?

IRMAA is driven by tax and income planning decisions, not by Medicare plan selection. Many professionals focus primarily on investments or insurance, while IRMAA planning requires coordination between taxes, retirement income, and charitable strategies. This type of integration typically falls under comprehensive financial planning.

The Bottom Line on Medicare Premium Surcharges (IRMAA)

Medicare IRMAA is one of the most expensive surprises retirees face because it often arrives after a one-time income spike.

With thoughtful planning, IRMAA exposure can often be anticipated, managed, and reduced, but it requires coordination between Medicare planning, tax strategy, and retirement income planning.

Want Help Managing Medicare IRMAA Exposure?

At White Cloud Wealth Management, we help retirees coordinate:

- Roth conversion strategy

- RMD and IRA withdrawal planning

- charitable giving (QCDs, donating stock, DAF strategies)

- capital gains timing

So Medicare premiums don’t become an unnecessary wealth transfer.

By Jacob Nye, Wealth Management Advisor/ CFP®

Disclosure

This blog reflects the personal opinions, viewpoints and analyses of the White Cloud Wealth Management employees providing such comments, and should not be regarded as a description of advisory services provided by White Cloud Wealth Management. The views reflected in the blog are subject to change at any time without notice. Nothing in this material constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security.